18 January, 2024

“While too early to predict exactly how consumers were impacted over the festive season, the start of 2024 will likely be challenging for retailers, with households clearly under severe strain,” says Johan Gellatly, MD of Altron FinTech.

The results of the latest Altron FinTech Household Resilience Index (AFHRI) were released today, showing that South African households remain under severe financial pressure, mainly as a result of the restrictive monetary policy stance by the South African Reserve Bank (SARB). The ratio between household disposable income and household debt costs is the worst-performing indicator.

MD of Altron FinTech, Johan Gellatly, believes the latest AHFRI results do not bode well for household consumption spending during the first quarter of 2024, especially after the December holiday period, when personal credit facilities are often stretched to their limits.

“While it is too early now to determine how consumers were impacted over December, we are of the view that the start of the year may be tough for retailers across the board, with households clearly under strain, especially those in the lower income brackets.”

Gellatly adds the AFHRI remains a key source of economic analysis, providing important benchmarking information to the market. “It also keeps us abreast of market trends, and in this way, we are able to continue providing customers with solutions that are effective and fit-for-purpose. Importantly, our solutions must enable customers to continue to trade effectively in a tough economic climate.”

According to economist Dr Roelof Botha, who compiles the index on behalf of Altron FinTech, a strong – and predictable – inverse correlation exists between higher interest rates and the AFHRI trend. “Over the past two years, the country’s benchmark prime lending rate has been raised consistently to almost 12% – the highest level in 14 years. This is despite the fact that the consumer price index is comfortably within the SARB’s target range for inflation of 3% to 6%, and that there are clear signs that inflationary pressures have receded since the second half of 2023.”

Botha points out that first-time home buyers have been particularly hampered by the high interest rates. The average deposit required for a bond for first-time home buyers (as administered by BetterBond) has shot up from 8.2% in 2019 to 14.7% last year. There has also been an increase in credit impairments by the banking sector

Predictably, the ratio between household disposable income and household debt costs has been the worst-performing indicator included in the AFHRI. “After increasing consistently since 2016, this ratio took a hefty knock in the second quarter of 2020 induced by the COVID-19 lockdowns, but then quickly recovered to a multi-year high. The reciprocal of this ratio, ie, debt costs to income, has risen from a low of 6.7% in the fourth quarter of 2021 to 8.9% in the third quarter of 2023 – an increase of some 33%,” says Botha.

“On a positive note, the decline in South Africa’s long-term bond yield of 120 basis points over the past three months is a clear indication the global and domestic capital markets are anticipating a drop in money market rates in the near future – hopefully in the first quarter of 2024.”

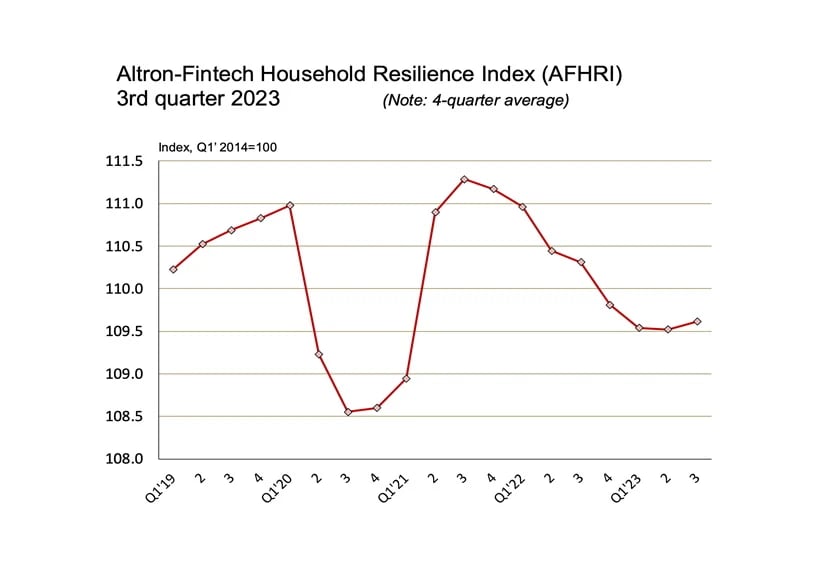

In the third quarter of 2023, the AFHRI recorded a value of 109.9, a marginal increase compared to the level of 109.1 during the second quarter of the year. No meaningful change was recorded year-on-year, although signs have emerged that the AFHRI has reached a trough.

Botha says lower interest rates will almost certainly lead to a new growth trend for the AFHRI, but the lingering effects of higher debt levels and subdued wage growth will be felt during the first half of 2024.

“Since 2014, the average annual improvement in the index is less than 1%, which serves as a clear indication of the economy’s underperformance, mainly because of low investor and business confidence resulting from state capture and the erosion of the efficiency of infrastructure. Over the past 18 months, this has been exacerbated by the negative effects of a sharp increase in the cost of credit.

The graph below illustrates the AFHRI trend based on a four-quarter average, which serves to eliminate seasonal variances. A pronounced recovery and new growth impetus occurred shortly after the worst of the COVID-19 period, but this was clearly halted in its tracks and then reversed by the restrictive monetary policy of the SARB.

The AFHRI trend based on a four-quarter average, which serves to eliminate seasonal variances.

Other salient trends include the following:

- Significant growth in employment in both the private and public sectors has provided a welcome buffer to the downward trajectory of the AFHRI. Unfortunately, private sector salaries have not matched the growth in jobs and continue to decline in real terms.

- The year-on-year decline in real household disposable income is a result of the unfortunate combination of relatively high inflation, lower real wages in the private sector and the increased debt repayment costs forced on households by the highest interest rates in 14 years.

- Credit impairments by banks continue to exert a downward impact on the AFHRI, representing the worst performing indicator since the pre-COVID-19 era.

The table on the following page summarises the performance of the different indicators comprising the AFHRI over four different periods, namely: since the base period of 2014; since the last comparable quarter before the COVID-19 lockdowns kicked in (Q3 2019); quarter-on-quarter; and year-on-year (percentage changes in real terms). The period since the third quarter of 2019 is regarded as relevant to gauge whether the financial resilience of households has fully recovered from the pandemic or not.

.webp?width=904&height=799&name=unnamed%20(1).webp)

Performance of the different indicators comprising the AFHRI.

In recognising the need for data that provides more clarity on the financial disposition of households in general, and their ability to cope with debt in particular, Altron FinTech commissioned Dr Botha, economist and economic advisor to the Optimum Investment Group, to assist in designing this index.

The index comprises 20 different indicators, all of which are directly or indirectly related to sources of income or asset values. The AFHRI is weighted according to the demand side of the short-term lending industry and calculated on a quarterly basis, with the first quarter of 2014 being the base period, equalling an index value of 100. All of the indicators are expressed in real terms, ie, after adjustment for inflation.